2020-VIL-03-AAR-DT

AUTHORITY FOR ADVANCE RULINGS - MUMBAI BENCH

A. A. R. Nos. 1555, 1556, 1557, 1558, 1559, 1560, 1561, 1562, 1563 and 1564 of 2013

Date: 18.03.2020

Name of the Applicant: COPAL PARTNERS LTD. (AND OTHER APPLICATIONS)

For the Applicant : Rajan Vora and Rishab Jalan , Chartered Accountants

For the Department : Smt. S. Padmaja , Commissioner of Income-tax, Departmental representative, and K. V. Aravind , Special Counsel

BENCH

G. Chockalingam J. (Vice-Chairman), Kishore Kumar Vyawahare Member Revenue And Inder Kumar Member Law

ORDER

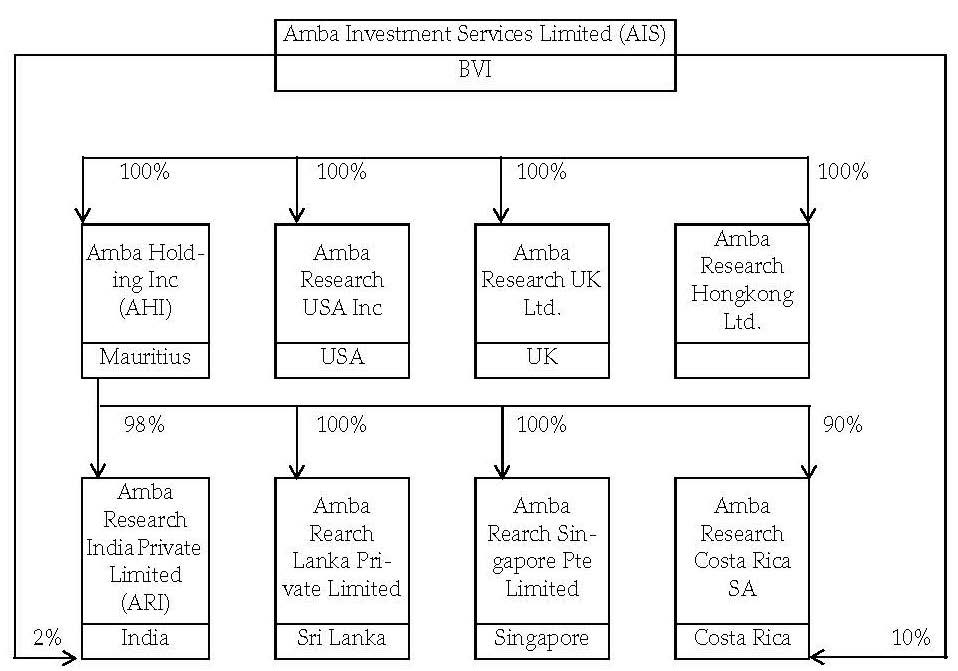

2. Moody's Analytics Knowledge Services (Jersey) Limited (earlier known as Copal Partners Limited and called "buyer" here), is a company incorporated under the laws of Jersey with its registered office at Ogier House, the Esplanade, St. Helier, Jersey JE4 9WG. It purchased the whole of the share capital of Amba Investment Services Limited ("AIS"), a private limited company, under the laws of the British Virgin Islands ("BVI"). AIS was converted into a public limited company with effect from July 1, 2013 by making the necessary amendments to the memorandum of association and the articles of association. AIS is the parent company of a multi-national group of companies having operations across Sri Lanka, Cost Rica, Singapore, India, US, UK and Hong Kong, whose structure is provided below :

3. ARI is a subsidiary of AHI. ARI is a private limited company, incorporated under the Indian Companies Act, 1956. The applicant has purchased the entire shareholding of AIS. At annexure-III, to the application of the buyer, it is indicated that it has purchased shares from 10 shareholders. Nine applicant sellers have filed applications before AAR. One Mr. Gilles Raoul Schuddeboom has not filed application before AAR but is mentioned in the application of Copal Partners Limited, Jersey USA and has maximum shareholding during the 12 months preceding the transfer of 0.33 per cent. of AIS shares. AIS had other shareholders apart from ten indicated above but they are not subject matter of applications filed. Nine "applicant sellers" are listed below :

|

Sl. No. |

Name of the shareholders |

No. of shares in AIS on the date of transfer |

% of shares in AIS on the date of transfer |

Maximum per cent. during the 12 months preceding the transfer |

Status |

Country |

|

1 |

Ana Gomez Chapman |

10,564 |

0.19 per cent. |

0.19 per cent. |

Individual |

USA |

|

2 |

David William James Garrett |

6,000 |

0.11 per cent. |

0.11 per cent. |

Individual |

UK |

|

3 |

Michael Joseph Morierty |

326,428 |

Less than 5 per cent.* |

6.02 per cent. |

Individual |

USA |

|

4 |

Johan Bertil Wissinger |

105,000 |

1.86 per cent. |

1.90 per cent. |

Individual |

USA |

|

5 |

Mary Gerard Berner |

163,214 |

2.89 per cent. |

3.01 per cent. |

Individual |

USA |

|

6 |

Michael John Millar |

6,780 |

0.12 per cent. |

0.13 per cent. |

Individual |

UK |

|

7 |

Pacific Ace Development Limited |

28,571 |

0.51 per cent. |

0.53 per cent. |

Foreign company |

Hong Kong |

|

8 |

Seowyan Investments |

91,035 |

1.61 per cent. |

1.68 per cent. |

Foreign company |

Cayman Islands |

|

9 |

Shirley Renwick |

43,705 |

0.77 per cent. |

0.81 per cent. |

Individual |

UK |

|

* At the beginning of the 12 months prior to the date of transfer, Michael Joseph Moriarty was holding 6.02 per cent. in Amba BVI (as shown in the table above). However, as on the date of transfer (i.e. December 10, 2013), the shareholding of Michael Joseph Moriarty is less than 5 per cent. in AIS. All the Transferors are non- residents as per section 6 of the Act. |

4. Analytics Knowledge Services (Jersey) Limited (earlier known as Copal Partners Limited) (AAR/1555/2013) has sought ruling on the following questions :

"(i) As the shares of AIS directly and indirectly derive less that 50 per cent. of their value from assets located in India, whether the income arising to the persons specified in Annexure III from the trans fer of shares in AIS to the applicant would be subject to tax in India ?

(ii) Whether income arising to Pacific Ace Development Limited and Seowyan Investments, being foreign companies, from the trans fer of shares in AIS to the applicant can be assessed to tax under section 115JB of the Act ?

(iii) Whether the applicant can be treated as a representative asses see as contemplated under section 160(1)(i) read with section 163 of the Act of the persons specified in Annexure II in respect of income arising to the said persons from the sale of shares in AIS to the applicant ?

(iv) Whether the applicant is required to withhold tax under section 195(1) of the Act in respect of the income arising to each of the persons specified in Annexure III upon transfer of shares in AIS to the applicant ?

(v) If the answer to question No. 4 is in the affirmative, what is the rate (before applying surcharge and cess) at which the applicant would be required to withhold taxes under section 195(1) of the Act on income arising to-

(a) individuals who have held the shares in AIS as short-term capital assets, from transfer of shares in AIS to the applicant ; and

(b) individuals and corporates who have held the shares in AIS as long-term capital assets, from transfer of shares in AIS to the applicant ?

(vi) Where the answer to question No. 4 is in the affirmative, whether the applicant is required to withhold tax at the higher rate specified under section 206AA(1) of the Act in respect of those per sons who have transferred shares in AIS to the applicant ?

(a) Who furnish their Permanent Account Number to the applicant on a date subsequent to the date the shares in AIS were transferred to the applicant ?

(b) Who do not hold a Permanent Account Number, and are thereby unable to furnish the same to the applicant ?"

5. In AAR/1556/2013 to AAR/1564/2013 ruling is initially sought below mentioned two questions :

"I. As the shares of AIS directly arid indirectly derive less than 50 per cent. of their value from assets located in India, whether the income arising to the applicant upon transfer of shares in AIS would be subject to tax in India ?

II. If the answer to question No. 1 is in the affirmative, what is the rate at which the income arising to the applicant upon transfer of shares in AIS would be subject to tax in India ?"

6. After filing of applications in December 2013, the Finance Act, 2015 introduced Explanations 6 and 7 to section 9(1)(i) of the Income-tax Act, 1961 ("Act") to clarify the particular situations to which Explanation 5 to section 9(1)(i) of the Act would apply. In the light of the aforesaid amendments, the sellers and the buyer filed two additional questions to the application on September 4, 2015. The two additional questions are :

I. Whether, having regard to Explanation 7(a) to section 9(1)(i) of the Act, the income arising to the applicant upon transfer of shares of AIS would be taxable in India where the applicant-

(i) Along with her associated enterprises, did not hold voting power, share capital or interest in AIS, AHI or ARI in excess of five per cent. at any time during the 12 months preceding the date of transfer of shares of AIS ; and

(ii) Along with her associated enterprises has not held the right of management or control in, or in relation to, AIS or AHI or ARI, at any time during the 12 months preceding the date of transfer of shares of AIS.

II. Without prejudice to other questions whether in terms of Explanation 7(b) to section 9(1)(i) of the Act, only such part of income as is attributable to assets located in India would be taxable in the hands of the applicant upon transfer of shares of AIS ?

7. Further question No. 1 of all applications were modified and substituted by the following question :

Modified question No. 1

"Whether the understanding of applicant is correct that in order to attract Explanation 5 to section 9(1)(i) of the Act, the threshold for determining value derived "substantially from the assets located in India" is 50 per cent. or more keeping in view the language as well as the intent of the said Explanation 5, which is further reflected in the clarificatory amendment introduced by Explanation 5, which is further reflected in the clarificatory amendment introduced by Explanation 6 to section 9(1)(i) of the Act and as has been held by the hon'ble Delhi High Court in the case of DIT (International Taxation) v. Copal Research Ltd. [2015] 371 ITR 114 (Delhi) (W. P. No. 2033 of 2013) dated August 14, 2014 and the hon'ble Authority for Advance Rulings in the case of GEA Refrigeration Technologies GmbH, In re [2018] 401 ITR 115 (AAR) ?"

8. Furthermore question No. 2 of seller applicants was modified as under - If the applicant were to be chargeable to tax in India, what is the rate at which the income arising to the applicant upon transfer of shares in AIS would be subject to tax in India ?

9. All original/modified or amended questions can be effectively merged into following relevant questions which will be answered by the authority :

"I. Whether clarificatory amendment introduced by Explanation 6 and Explanation 7 to section 9(1)(i) of the Act have retrospective operation ?

II. If the answer to question No. 1 is in the negative as the shares of AIS directly and indirectly derive less than 50 per cent. of their value from assets located in India, whether the income arising upon trans fer of shares in AIS would be subject to tax in India ?

III. If the answer to question No. 2 is in the affirmative, what is the rate at which the income arising to the applicant upon transfer of shares in AIS would be subject to tax in India ?

IV. Whether, having regard to Explanation 7(a) to section 9(1)(i) of the Act, the income arising to the seller applicant upon transfer of shares of AIS would be taxable in India where the seller applicant-

(i) Along with her associated enterprises, did not hold voting power, share capital or interest in AIS, AHI or ARI in excess of five per cent. at any time during the 12 months preceding the date of transfer of shares of AIS ; and

(ii) Along with her associated enterprises has not held the right of management or control in, or in relation to, AIS or AHI or ARI, at any time during the 12 months preceding the date of transfer of shares of AIS.

V. Without prejudice to other questions whether in terms of Explanation 7(b) to section 9(1)(i) of the Act, only such part of income as is attributable to assets located in India would be taxable in the hands of the applicant upon transfer of shares of AIS ?

VI. Whether income arising to Pacific Ace Development Limited and Seowyan Investments, being foreign companies, from the trans fer of shares in AIS to the applicant can be assessed to tax under section 115JB of the Act ? If yes, whether the buyer applicant can be treated as a representative assessee as contemplated under section 160(1)(i) read with section 163 of the Act of the persons specified in annexure II in respect of income arising to the said persons from the sale of shares in AIS to the applicant ?

VII. Whether the seller applicants are required to withhold tax under section 195(1) of the Act in respect of the income arising upon transfer of shares in AIS to the buyer applicant and if yes at higher rates in appropriate cases ?"

Applicant's contentions

10. The learned authorised representative has stated that the Finance Act, 2012 inserted a deeming provision by way of Explanation 5 to section 9(1)(i) of the Act (hereinafter referred to as "indirect transfer provisions"), which reads as follows :

"For the removal of doubts, it is hereby clarified that an asset or a capital asset being a share or interest in a company or entity registered or incorporated outside India shall be deemed to be and shall always be deemed to have been situated in India, if the share or interest derives, directly or indirectly, its value substantially from the assets located in India."

Under the above deeming provisions, a share in a company incorporated outside India shall be deemed to be situated in India if the share or interest derives, directly or indirectly, its value "substantially" from the assets located in India.

11. It is submitted that post-introduction of the indirect transfer provisions by the Finance Act, 2012 vide Explanation 5, there were numerous issues regarding the interpretation and applicability of said indirect transfer provisions. In this context, the Government constituted an Expert Committee, under the Chairmanship of Dr. Parthasarathi Shome to provide recommendations for addressing issues pertaining to the indirect transfer provisions. The expert Committee made a number of recommendations to bring in clarity regarding the scope and impact of the indirect transfer provisions. Subsequently, the Finance Act, 2015 introduced a number of amendments to the Act, in order to give effect to the Expert Committee's recommendations. These amendments were introduced in the form of "Explanations" to section 9(1)(i), explaining the scope and impact of the indirect transfer provisions.

12. It is argued that since these amendments provided the necessary machinery provisions in the absence of which implementation of the indirect transfer provisions as set out in Explanation 4 and 5 to Explanation 7 to section 9(1)(i) they should be applied with retrospective effect.

13. Further, it is submitted that whenever there is any ambiguity in interpretation of law and to remove the said ambiguity, any amendment is proposed by Parliament, even if prospectively, then the same should be treated as remedial in nature, designed to eliminate unintended consequences which may cause undue hardship to taxpayers, the same should be construed as retrospective in operation. In this regard, reliance is placed on the hon'ble Supreme Court decision in the case of Allied Motors (P.) Ltd. v. CIT [1997] 224 ITR 677 (SC) and the decision of the apex court in the case of CIT v. Alom Extrusions Ltd. [2009] 319 ITR 306 (SC).

14. It is urged that applying the above principle to the facts of the case under consideration, the applicant is only praying for a ruling on retrospective applicability of Explanation 6 (i. e., Explanation 6 to be read with Explanation 5), to state that the word "substantially" used in Explanation 5 is defined to mean threshold of 50 per cent. and more and request for directions that in case the value of assets in India is less than 50 per cent., nothing will be taxable in India on account of such indirect transfer and therefore, the sellers mentioned in Authority for Advance Rulings application number No. 1556 of 2013 to 1564 of 2013 and Gilles will not be taxable in India.

15. Since the applicant is only seeking a ruling on the principle of whether Explanation 6 to section 9(1)(i) of the Act is applicable to the said transfer of shares in AIS the applicant has not asked for a ruling on the valuation of assets attributable to India operations, although in the application, a valuation report obtained from an independent valuer is enclosed as per which the value of shares of AIS derived directly or indirectly from assets located in India is 26.38 per cent. Thus, it is submitted that the hon'ble Authority for Advance Rulings may pass the appropriate orders on the principles involved alone, since the Department would have the opportunity to examine the valuation report produced by the applicant during assessment proceedings.

16. It is also indicated that irrespective of whether the shares of AIS derive, directly or indirectly its value "substantially" from the assets located in India, Explanation 7(a) to section 9(1)(i) of the Act should be applicable, which provides that where the transferor who along with his/her/its associated enterprises, has not held any voting power, share capital or interest in the foreign company whose shares are transferred in excess of 5 per cent. nor any right of management or control in such foreign company during the twelve months preceding the date of transfer, the income from transfer of shares of such foreign company for such transferors would not be taxable in India.

17. To substantiate that the eight sellers (except Michael Joseph Morierty, USA) satisfy the conditions prescribed in Explanation 7(a), vide submission dated December 27, 2019, a copy of the confirmation from the sellers (or their representative) that the seller (along with his/her/its associated enterprises) neither held any voting power, share capital or interest in Amba Mauritius or Amba India in excess of 5 per cent. nor any right of management or control in Amba BVI, Amba Mauritius and Amba India during the twelve months preceding the date of transfer, i. e., December 10, 2013 along with copy of extract of the register of members of Amba BVI along with summary of shareholding was filed.

18. In continuation of his arguments, learned authorised representative has prayed that Explanation 7(b) (which was also introduced into the statute by the Finance Act, 2015 under the same category of being "clarification" relating to indirect transfer provisions as Explanation 6) is also to be applied retrospectively.

19. Without prejudice to what is stated above, it is submitted that Explanation 7(b) addresses the concern of taxpayers to clarify that, where the foreign company holds other assets outside India besides assets located in India, only reasonably attributable to asset located in India will be taxable in India. It is pleaded that there does not seem to be a reason why Legislature would have wanted taxation of the whole of the gains (rather than gains reasonably attributable to asset located in India). In similar cases of transfer described in Explanation 7(b) prior to the insertion of the said Explanation, additionally, there could also be a question of "sufficiency of nexus with India" with respect to the portion of gains not attributed to India assets, if this Explanation were not to be operative for past periods.

20. On the issue of applicability of section 115JB of the Act for Pacific Ace Development Limited and Seowyn investment, it is stated that Explanation 4 was inserted to section 115JB by the Finance Act, 2016 with retrospective effect from April 1, 2001. The said Explanation 4 provides as follows :

"For the removal of doubts, it is hereby clarified that the provisions of this section shall not be applicable and shall be deemed never to have been applicable to an assessee, being a foreign company, if-

(i) the assessee is a resident of a country or a specified territory with which India has an agreement referred to in sub-section (1) of section 90 or the Central Government has adopted any agreement under sub-section (1) of section 90A and the assessee does not have a permanent establishment in India in accordance with the provisions of such agreement ; or

(ii) the assessee is a resident of a country with which India does not have an agreement of the nature referred to in clause (i) and the assessee is not required to seek registration under any law for the time being in force relating to companies." (emphasis supplied).

21. The above Explanation makes it clear that section 115JB of the Act is not applicable to foreign companies satisfying conditions prescribed in clauses (i) and (ii) of Explanation 4 to section 115JB to the Act.

22. It is highlighted that :

(a) Both Pacific Ace Development Limited and Seowyan Investments are foreign companies and do not have any permanent establishment or business connection in India.

(b) During the financial year 2013-14 (year covering the date of transfer), both Pacific Ace Development Limited and Seowyan Investments did not have any presence or place of business in India.

(c) During the financial year 2013-14 (year covering the date of transfer), both Pacific Ace Development Limited and Seowyan Investments were not required to seek registration under the Companies Act, 2013, Companies Act, 1956 or any law for the time being in force relating to companies in India.

23. It is thus argued that since the conditions discussed above are not met in the case of both Pacific Ace Development Limited and Seowyan Investments, income arising to both Pacific Ace Development Limited and Seowyan Investments being foreign companies cannot be assessed to tax under section 115JB of the Act.

Revenue's contentions

24. The learned Departmental representative has mentioned that it is evident that the assessee has no objection that the receipt accrues or arises in India in the hands of the transferors. The only contention of the assessee is that the sum would not be taxable since the shares of AIS do not derive their value substantially from asset located in India.

25. Drawing attention to the valuation report submitted by the applicant, it is submitted that from the valuation report (page No. 6, in section 2 background of overview on ARI submitted by the applicant) furnished by the applicant, it can be inferred that, the revenue Growth of the Moody's Analytics Knowledge Services (India) Private Limited (formerly known as Amba Research India Private Limited, from the financial years 2014-15 to 2017-18, was projected to be on a reducing trajectory, from 24 per cent. in 2015 to 17 per cent. in 2018. However, the return of income of the Moody's Analytics Knowledge Services (India) Private Limited shows that, the revenue growth as per actuals are in a progressive trajectory, as shown in the following table :

|

Particulars |

AY 2014-15 |

AY 2015-16 |

AY 2016-17 |

AY 2017-18 |

AY 2018-19 |

|

EBDITA |

30,96,99,705 |

22,28,14,643 |

25,07,45,431 |

28,78,79,711 |

32,11,45,168 |

|

Operating revenue |

119,13,69,064 |

121,10,91,665 |

121,69,15,789 |

145,66,39,498 |

160,88,02,978 |

|

Capital expenditure |

72,63,379 |

27,27,530 |

4,65,20,932 |

2,75,63,615 |

2,18,97,197 |

26. From the above comparison of the DCF report furnished by the applicant based on the valuation, and with the actual revenue growth, as per the return of income filed by Moody's Analytics Knowledge Services (India) Private Limited (formerly known as Amba Research India Private Limited), it is clear that the valuation methodology adopted by the applicant over valuation of the enterprise, is to project a lesser value to the Indian entity. As seen from the above, it is clear that the revenue and revenue growth as adopted in valuation report are in contrast with that as per ITR. Further there is no detailed explanation for such projection adopted in valuation report. This finding alters the basic assumptions/projections made in respect of the ARI and thus its enterprise value cannot be accepted as determined in the said report. On the same basis, it cannot be concluded that the enterprise value of the ARI vis-a-vis AIS is less than 50 per cent. or is not substantial. In this case as the value of asset located in India is considerably high as compared to other global subsidiaries, it is very much clear that AIS shares derive their value directly or indirectly substantially from assets located in India and the receipt would therefore be taxable in India.

27. Further, it is emphasised by the learned special counsel that Explanation 6 and Explanation 7 inserted by the Finance Act, 2015 are applicable prospectively that is from April 1, 2016 and thus are not applicable to the applicants.

28. Referring to Explanation 7 to section 9(1)(i) of the Act it is stated that the applicant has not submitted any document to the effect that the shareholding of any of the non-resident along with its associated enterprise is below 5 per cent. For application of this clause, the shareholding pattern of individuals along with associated enterprises as per section 92A should be less than 5 per cent.

29. It is also submitted in the report of the Revenue that the Finance Act, 2016 inserted Explanation 4 to section 115JB, which is with effect from April 1, 2001 and from Explanation 4 to section 115JB, it is very much clear that section 115JB is applicable to the foreign company which have a permanent establishment in India. From the material available on record and submissions made by the applicant, the Assessing Officer is not in a position to determine whether the above mentioned foreign companies are having permanent establishment or not. Permanent establishment depends on various factors and a detailed study of the activity of the foreign companies in connection of India is required to arrive at any conclusion.

30. It is also indicated in the report that the applicant has acquired the shares of AIS which is ultimate holding of ARI, having all asset situated in India. Hence in the context of section 160(1)(i) read with section 163(1)(d) the applicant is liable to be treated as representative assessee for AIS. It is also hereby submitted that as per section 163(2), the applicant would not be treated as agent without affording an opportunity of being heard by the Assessing Officer.

31. Lastly, it is mentioned that from the plain reading of the section 195(1), it is very much clear that the sum which is chargeable to tax in India is subject to tax at source while making payment or credit to the account of payee, whichever is earlier. In this instant case, as discussed above, the sum received/receivable for sale of share is liable to tax in India hence the same is subjected to tax at source at applicable rate as per Income tax Act.

32. We have carefully considered the contentions of the learned authorised representative, the report of the Revenue and the arguments of the learned special counsel. The only germane issue is whether Explanation 6 and Explanation 7 inserted by the Finance Act, 2015 to section 9(1)(i) of the Income-tax Act are retrospective or prospective in nature.

33. It is a fact that during 2012 to 2016, the word "substantially" appearing in Explanation 5 was not defined in the Act and it was subject matter of scrutiny of the courts in a number of cases, i. e., DIT (International) v. Copal Research Limited (supra), GEA Refrigeration Technologies GmbH (supra) and Banca Sella S. P. A., In re [2016] 387 ITR 358 (AAR) and it was uniformly held that "substantially" will mean at least 50 per cent. This position was also clarified by Explanation 6 which was brought into statute after recommendation of Expert Committee under Dr. Shome on this issue was accepted by Government and Circular No. 19 of 2015, dated November 11, 2015 affirmed this position.

34. Further the language of Explanation 6 begins with words "for the purposes of this clause it is hereby declared. . . "in Justice G. P. Singh's (Sixth Edition 1996) "Principles of Statutory Interpretation" under the heading "declaratory statutes", the learned author has summed up as under :

"Declaratory statutes : The presumption against retrospective operation is not applicable to declaratory statutes. As stated in Craies and approved by the Supreme Court : 'For modern purposes a declaratory Act may be defined as an Act to remove doubts existing as to the common law, or the meaning or effect of any statute. Such Acts are usually held to be retrospective. The usual reason for passing a declaratory Act is to set aside what Parliament deems to have been a judicial error, whether in the statement of the common law or in the interpretation of statutes. Usually, if not invariably, such an Act contains a preamble, and also the word 'declared' as well as the word 'enacted'. But the use of the words 'it is declared' is not conclusive that the Act is declaratory for these words may, at times, be used to introduce new rules of law and the Act in the latter case will only be amending the law and will not necessarily be retrospective. In deter mining, therefore, the nature of the Act, regard must be had to the substance rather than to the form. If a new Act is 'to explain' an earlier Act, it would be without object unless construed retrospective. An explanatory Act is generally passed to supply an obvious omission or to clear up doubts as to the meaning of the previous Act. It is well-settled that if a statute is curative or merely declaratory of the previous law retrospective operation is generally intended. The language 'shall be deemed always to have meant' is declaratory, and is in plain terms retrospective. In the absence of clear words indicating that the amending Act is declaratory, it would not be so construed when the pre-amended provision was clear and unambiguous. An amending Act may be purely clarificatory to clear a meaning of a provision of the principal Act which was already implicit. A clarificatory amendment of this nature will have retrospective effect and, therefore, if the principal Act was existing law when the constitution came into force, the amending Act also will be part of the existing law."

35. We are thus in agreement with the view of learned authorised representative that Explanation 6 is clarificatory in nature and would apply retrospectively. Similarly, Explanation 7 inserted to address the genuine concerns of small shareholders would also apply retrospectively to give meaning in true sense and to render indirect transfer provisions contained in Explanation 5 to section 9(1)(i) of the Income-tax Act workable.

36. The learned authorised representative has indicated that as per the valuation report obtained from the independent valuer the value of shares of AIS derived directly or indirectly from assets located in India is 26.38 per cent., i. e., less than 50 per cent. In view thereof the income from transfer of shares in the hands of transferors is not subject to tax in India.

37. It is noticed that the applicants and Seowyan Investments are based in Cayman Islands with whom India does not have comprehensive DTAA. Also, in the case of Pacific Ace Development Limited, a resident of Hong Kong with whom the comprehensive DTAA came into force in respect of income derived in India with effect from April 1, 2019. Learned authorised representative had asserted that during the financial year 2013-14 both the foreign companies are not required to seek registration under the Companies Act, 2013, Companies Act, 1956 or any other law for the time being in force relating to companies in India. In view of the said averments by learned authorised representative and also considering the provisions of section 115JB of the Income-tax Act, the conditions laid down in section 115JB are satisfied and there is no applicability of section 115 to the above referred foreign companies. Consequently, there is no liability, the buyer applicant is not required to withhold taxes in respect to the payment made to transferor of shares.

38. Considering that the Revenue had questioned the valuation methodology, the Revenue may verify the computation furnished by the applicant as per rule 11UB and rule 11UC. It is reiterated that the ruling is given on matter of principle, i. e., retrospective/prospective application of Explanations 6 and 7 and based on the figures presented before us by learned authorised representative. If subsequently it is found that the figures are at variance and the actual percentage exceeds 50 per cent., the ruling would not apply and the Revenue would not be bound by such ruling. If it is found that the actual percentage is more than 50 per cent. then the Revenue may also ascertain the shareholding of each of the seller applicants at any time in 12 months preceding the date of transfer and/or the right of management or control in relation to AIS and thereafter if need be ascertain the income reasonably attributable to non-resident transferors in terms of Explanation 7(a) and 7(b) to section 9(1)(i) of the Income-tax Act. Further, if it is discovered later on that the conditions laid down in 115JB are not satisfied the transferor foreign companies would be subject to section 115JB.

39. For the reasons mentioned above, the ruling in respect of effective questions raised in the cases of all the applicants is as under-

- Questions Nos. I and II - Explanations 6 and 7 to section 9(1)(i) of the Income-tax Act are clarificatory in nature and would apply retrospectively and therefore the incomes from transfer of shares in the hands of transferors are not subject to tax in India.

- Questions Nos. III to V - Does not arise in view of reply to I and II above

- Question No. VI - Section 115JB is not applicable to Seowyan Investments and Pacific Ace Development Limited.

- Questions No. VII - There is no liability under section 195 of the Income-tax Act of the Moody's Analytics Knowledge Services (Jersey) Limited to withhold taxes in respect to the payment made to transferor of shares.

DISCLAIMER: Though all efforts have been made to reproduce the order accurately and correctly however the access, usage and circulation is subject to the condition that VATinfoline Multimedia is not responsible/liable for any loss or damage caused to anyone due to any mistake/error/omissions.